COVID crisis left your family business facing insolvency? What to do…

If the COVID crisis has left you approaching insolvency, you must take the right actions (if unsure, see our 17 indicators of insolvency). This article will walk you through what to do, in the right order, to help you turn your business around. But before I get into the hows-and-wherefores, let’s think a little bit about the impact of the economy.

Even the best businesses experience changes and disruption during an economic downturn. It’s important that you understand what is going on, how to read it, and how to make a decision for yourself.

WARNING: You must be willing to think about the worst-case scenario, and to play the long game.

If you are, you’ll find this article both useful and helpful.

Let’s get started…

The economy really does have an impact

The impact of the COVID crisis can divert your attention from broader economic trends, but those trends really do matter. Some have claimed that there’s no empirical model to ascertain whether or not we’re headed into a recession or depression – but there is!

All you have to do is look at economic indicators in the months before COVID, and in the same period in the year before. And then step further back into history so you gain a complete picture, because short time-scales can be misleading. You can examine current and historical economic data at https://tradingeconomics.com/australia to do your own risk assessments.

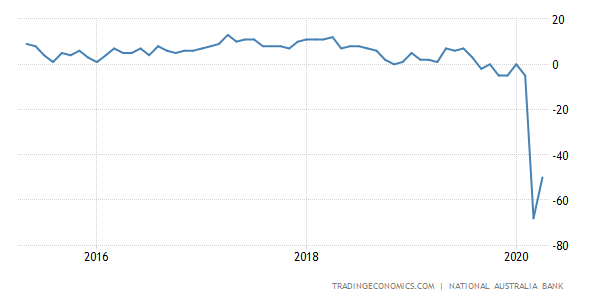

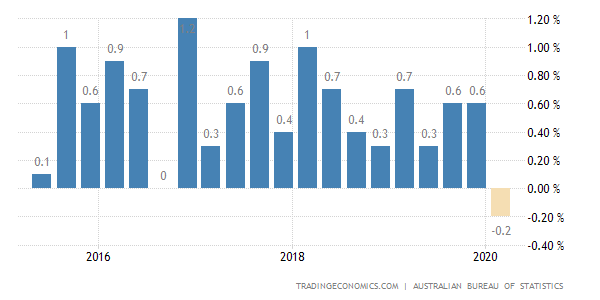

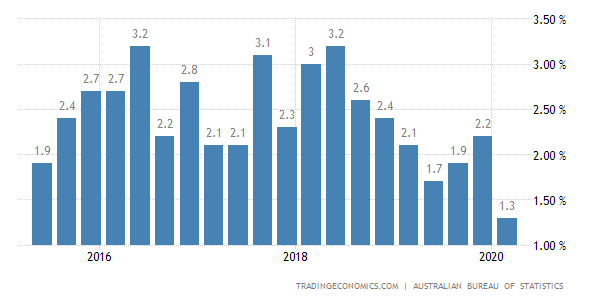

But if we were to take some highlights from Trading Economics, we would spot a number of downward trends.

- Business confidence is trending down:

- Consumer confidence is trending down:

- GDP Growth is trending down:

- Annual GDP Growth is trending down:

- Inflation is trending up:

- The Reserve Bank is printing money like there’s no tomorrow:

All of these are good indications that the economy is in a significant amount of trouble.

All sourced from: tradingeconomics.com

If you don’t know how to interpret economic data, here’s a basic primer

Investing extraordinaire Ray Dalio explains that you can predict downturns, recessions and depressions simply by understanding how the economy works.

You can watch his fantastic video above (it’s 30 mins long), but the basics are as follows:

The economy turns on debt, because debt fuels spending. As Dalio points out, ‘one man’s spending is another man’s income’. When things seem like they’re going really well, people borrow more, asset values go up, stocks go up, and it pays to buy things with borrowed money. But over time, debt repayments start growing faster than incomes. When one person’s spending is another person’s income, debt growth means that income values drop, and then borrowing drops.

And then the prosperity cycle reverses itself.

People cut spending, incomes fall, asset prices drop, the market feels the pressure. Borrowers can no longer borrow enough money to repay their debts, and so then they sell their assets. When this begins to happen, real estate prices drop, banks get squeezed, and the stock market tanks.

When businesses cut costs, people lose their jobs; then debts must be reduced; then eventually people rush the banks for their money… and that becomes a depression.

The same pattern has occurred in every major downturn.

The video explanation is much more detailed (and more interesting!) than mine, and I highly recommend watching it.

First, decide where you think the economy is going (post-COVID crisis)

Given Australia hasn’t had a recession since the early 1990s, and hasn’t had a depression for just shy of a hundred years, it would be safe to assume that nobody is qualified to advise you during a worst-case economic situation.

But there are some things that you must do if you’re going to come out on top.

They are:

- decide where you feel that the economy is going, and whether we are headed towards a recession or depression

- plan for a longer recovery period than you might reasonably expect

- plan to have to function in line with your Worst Case scenario option

- increase your productivity, which may mean being flexible or changing how you do things

- keep your income higher than your debts.

Then, take the right action!

There are a number of steps that you can take right now that will help you to decide whether to keep trading or close up shop.

But before I go into those, it’s worth knowing that the Commonwealth Government has taken the extraordinary step of allowing you to trade insolvent for six months (COVID19 Safe Harbour). That’s six months from the beginning of the COVID crisis; so it effectively runs out in September 2020 (you should be thinking of transitioning to the 2017 Safe Harbour prior to this as it affords ongoing protection and more options to restructure…).

Before September arrives, you’ve got time to reorganise and adapt your business and get it moving again. Of course, if you can’t do that, then you may be required to seek the advice of a registered liquidator and appoint a voluntary administrator.

Nevertheless, here is a comprehensive list of the actions that you can start taking now:

- Deal with root causes, and act in line with your proposed “worst case” scenario. Even though you are probably optimistic, if your thinking told you that you’re heading into a depression, act early. This means: Change your offerings, downsize, reduce overheads. Do whatever you have to do, and do it fast, and clean.

- Complete, and then carefully review, all of your financial data. Get your books up to date, and then apply short payment timeframes to everyone who owes you money. Conduct a clear analysis of your outgoings. In plain terms: If your house is falling down around your ears, what will you keep? Everything else you don’t need.

- Get rid of employees who aren’t performing. If you were to think about a new CEO coming into your business, the first thing he or she would do is to evaluate what’s working and what’s not… and they’d get rid of what isn’t working, including Keeping underperforming or poorly performing staff on your books isn’t good for your bottom line. As Ray Dalio would say, do whatever it takes to increase your productivity.

- Eliminate suppliers whose prices are too high. During the COVID financial crisis, your creditors are not able to demand payment. But as soon as this is over, they will. By looking to eliminate them, you may find yourself in a position to negotiate better terms, and thus come out on top in relation to any existing debt.

- Go hard after your target clients. In a time of crisis, your first criterion for your ideal client is, of course, the ability to pay. Analyse your client base: Are your best clients in the top 20%? What would happen to your financial resources if you could simply divest yourself of the remaining 80%? Run the thought experiment and see where it leads you.

- Avoid loans, especially if they’re expensive. Loans can be useful, but not when you’re just going to spend the money on overheads. The time to go for a loan is when you have a cashflow forecast, when you have a strategy for deploying the money, and when you are crystal clear about how the debt is going to turn into cashflow.

- Plan for your recovery. After most of your team has been successfully working from home, and you’ve adapted to new methods, will you want to go back to the way it was? Chances are good that you’ve discovered new ways to be effective, different efficiencies, and more valuable methods. Embrace those, and plan to embed them moving forward. The person who thinks they can abandon these is more of a fool than he realises.

- Keep your cash up, even if you don’t have to. If you’re not able to recover debts, find a way at least to preserve your existing cash position. This is important if you’re unable to evict tenants, for example. In the long-run, those with cash will be better off.

- Change when it makes sense, not when you’re forced to. By this I mean that if something isn’t working, change your strategy instead of strangling your business. The best way to figure this out is to go after the high value opportunities. You can only spot those if you’re in touch with your customers, if know what’s going on in the market, and if you are able to position yourself to take advantage of those opportunities.

- Get professional advice. Even if you think that your changes might make professional advice irrelevant, seek it anyway! Gaining an objective opinion may be valuable. For example, if you have the opportunity to take advantage of the safe harbour from insolvent trading, it may be wise to do so early.

In summary

Australia’s economy is heading into a recession, if not a depression. The time to make change is now, but shifting your view requires both courage and creativity. You have plenty of both, or you wouldn’t be in the role you have today.

All you have to do to come out on top is to cut costs, keep your cashflow positive if possible, eliminate everything that you don’t need, be flexible with change, and get advice from a qualified and experienced professional.

This is why I provide free initial consultations to help you understand the best way to turn your business around. We’re located in Adelaide but offer free online consultations nationwide. Give me a call on 0439 189 236 today.

2 thoughts on “COVID crisis left your family business facing insolvency?”

Comments are closed.