The SME market has had it very tough in Australia – smaller and family businesses have struggled to avoid failure when faced with financial crisis. The former “one size fits all” approach to for assisting businesses in financial distress has been widely accepted as being flawed.

There is a significant difference between financially distressed large enterprises (for example, Whyalla’s steelworks and the recent Carillion collapse in the UK) to the smaller or family owned business that relies on a relatively small number of key customers, suppliers and financiers to remain profitable or even viable.

Failure

- Obviously, there are also peaks and troughs experienced by small and family owned businesses and these can be particularly hazardous (for example, where business is seasonal or where demand can easily fluctuate).

- With a large corporation, these may simply be considered ‘ups and downs’ or ‘temporary glitches’ and a whole host of fall back measures can be relied upon to restructure and realign the corporate set back so it retains its profitability.

- Basically, there are clearly huge differences between the governance and management of large enterprises and smaller or family sized businesses.

The bigger you are, the harder you fall…

Jim Collins is an author and had major successes with two best-selling business books of all time, Built to Last and Good to Great. However, then Collins turned to the ‘dark side’ (as he jokingly described it). Just prior to the economic disaster, Collins wrote a book on corporate failure ‘How the Mighty Fall and Why Some Companies Never Give In‘ . As some of the biggest and reputable corporations were crashing and burning, it was Collins who logically assumed to conduct postmortems for signs and clues as to what pulled them down.

The smaller you are, the deeper the wounds…

- In attempting to apply the above to smaller and family sized businesses, it becomes apparent that Stages 3 and 4 would occur over an extremely short timeframe. When compared to a large corporation, there just isn’t sufficient ‘wiggle room’ for you to use the same techniques and tools to rescue your business.

- In the blink of an eye, you have transitioned from a state of positiveness and optimism to a highly stressful position of business failure and, critically, personal liability. All of a sudden, your business now threatens those that rely on you – your suppliers, creditors and stakeholders.

- Worse still, there is a risk to your own personal reputation, happiness and the well-being of your family and dependants.

Inaccessibility of the Formal Rescue Procedures to Smaller and Family Businesses

- Restructuring in Australia may use a formal mechanism such as a scheme of arrangement, with major debt restructurings involving Nine Entertainment, Centro and Alinta using this model. However, creditor schemes remain relatively uncommon outside of very large and complex restructurings.

- There are just over 1,200 voluntary administrations each year with roughly 1/3 of those entering a deed of company arrangement which may be used to restructure or (more likely) to sell the business or its assets.

- Empirical research suggests that unsecured creditor returns for deeds of company arrangement are less than 6c in the dollar on a weighted average basis.

‘Safe Harbour’ and ‘Ipso Facto’ – Powerful Reforms

- Fortunately, the new reforms are introducing a powerful new framework to help salvage the business and assets of small and family owned companies facing financial distress and crisis.

- With the Treasury Laws Amendment (Enterprise Incentives No 2) Bill 2017, came a complimentary two-layered adjustment to the restructuring and turnaround landscape. A stay on the termination clauses of contracts (‘Ipso Facto’ clauses) is to be introduced in 2018.

- When coupled with directors’ access to Safe Harbour from insolvent trading personal liability (effective 19 September 2017), there now exists a framework for which small and family businesses can use in avoiding failure.

Rescue Regimes and Informal Workouts

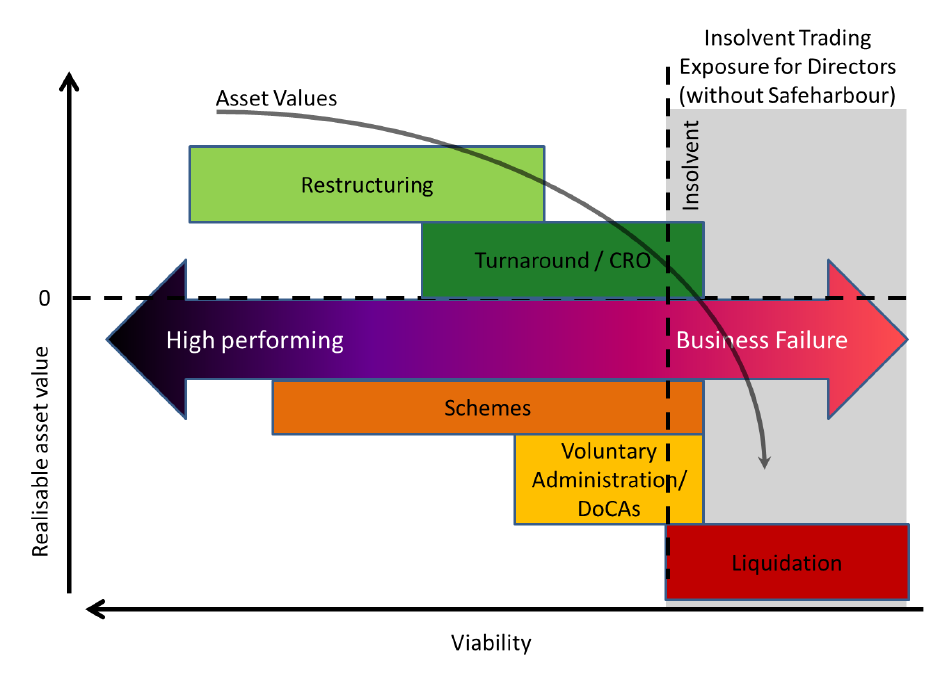

The two formal rescue regimes in Australia include a Scheme of Arrangement and Voluntary Administration. Creditors “schemes of arrangements are often criticised as being slow, costly, and cumbersome” (Jason Harris, 2017) and therefore inaccessible to smaller and family businesses. The value and viability of a business and assets quickly deteriorates – the above four scenarios provide an illustration of this through various points of sale (colour coded per above). This should be considered in conjunction with the ‘Value vs Viability’ diagram that follows:

- Voluntary Administration can lead to a proposed deed of company arrangement (DOCA). An agreement is made with creditors and the business can survive – whether in the hands of the same directors or an alternative mix of top management. However, as quoted above, approximately only 400 of the 1,200 administrations become a DOCA (most likely used to sell the business and assets – not return to control of the former management) and unsecured creditor returns are, on weighted average, less that 6%.

- If a Sale of the Business and Assets of the Company were to be effected, it would be ideal for this to occur at the earliest possible opportunity. At this point, there has been no public announcement that the business may be in distress or struggling financially and, therefore, the value in the ‘business’ (being it’s goodwill, assets, employees, supply chains etc) is maximised.

- A Sale of the Business and Assets can even be made during Administration by the Voluntary Administrator. Pursuant to section 437A a sale may provide for a better realisation to creditors and further minimise the claims of creditors with priority status (employees) or with registered security (for eg, a bank with a floating charge debenture).

- A Sale of the Business and Assets through Liquidation. By the time the company is in liquidation, the position has become far more terminal. The majority of employees, contractors and subcontractors have departed the picture. Furthermore, customers are sourcing elsewhere (there’s no time to wait for a speculative phoenix), stakeholders have lost all faith and often relationships are destroyed beyond repair. Also, regulatory or trade licenses are often automatically terminated.

Value vs Viability

Ideal Point to Involve a Turnaround Practitioner?

- Importantly, Safe Harbour can be implemented at any time during the business cycle. This is an extremely powerful factor as it means that start ups, which often struggle following their launch, will not only attract more experienced directors to their boards but also stand a great chance of enticing business angel investors, venture capitalists and private equity firms. The insolvency risks faced by start-ups are effectively reduced and directors compliance must be maintained to preserve the ongoing ‘safe harbour’ protection.

- Smaller and family businesses must take risks. Risk and strategy are interrelated and discussions or decisions by businesses concerning strategy, by definition, involve a discussion of risk. As with formal insolvency or rescue regimes, there is not a “one size fits all” risk management approach which can be taken by businesses. Even the leading standards on risk management recognise the need the risk frameworks to be tailored into a system that is appropriate to the needs of the business. The boards of larger companies make a point in determining their ‘risk appetite’, however, smaller and family businesses are unlikely to have such luxuries as time, resources or information that is readily available.

- It is our opinion, therefore, that all small and family businesses maintain dialogue with a turnaround practitioner throughout their entire life cycle (or rather, throughout their ‘journey’). In order for a business to achieve sustainable growth, risks must be taken and liaising with professionals (whether accountants, lawyers, advisors or turnaround practitioners) is an extremely useful habit to adopt. This doesn’t mean actual paying for advice – rather using the professionals as a sounding board prior to embarking on new projects, ventures, financing or recapitalisation.

‘Ipso Facto’ Clauses – Happy New Year 2018

- Another key part of the reform is the ‘Ipso Facto’ clause stay – this is aimed at preventing parties to a contract from terminating due to initiating a formal insolvency process (or taking steps to do so). Also, a contract is not able to be terminated simply due to the business’s financial position.

- Under existing laws when a business enters into administration it faces immediate value destruction as suppliers and large customers simply terminate contracts seal the fate of the business. The reform, to become effective in 2018, puts a stay on exercising ‘ipso facto’ clauses so that businesses in financial difficulty get some ‘breathing space’. There will be an opportunity to return the business to solvency or, if insolvency is suspected in the future, they may begin restructuring and turnaround.

- This is something to be cautious about when sitting on the other side of table. If your business supplies to a customer and they enter administration, you are no longer able to terminate the supply contract based on the terms contained within.

It should be noted that the Ipso Facto provisions are being grandfathered and will only apply to contracts entered into after commencement which will create different regimes and, in our opinion, will encourage parties to amend rather than enter into new contracts so as to retain the benefit of existing Ipso Facto rights.

Reassessing the term ‘Failure’…

- These new reforms stand to be of significant benefit to smaller and family businesses. The intention of Ipso Facto reform, expressed in the legislation and explanatory materials, is to give additional breathing space to continue trading whilst undertaking turnaround and restructuring – whether or not this is under safe harbour protection or through a formal rescue regime (such as voluntary administration and schemes of arrangement).

- In applying some practical perspective to the above illustrations, it is anticipated there will be an increase in the use of both safe harbour and informal workouts. The sheer threat of any formal insolvency rescue appointment, knowing that that would impose a stay on enforcing the contractual termination rights through ipso facto reform, will be sufficient incentive to enter into negotiations.

- Therefore, the term ‘failure’ needs to be reconsidered and viewed in a much broader context. Businesses in their early stages that do not yet have sufficient capital or are deemed too ‘risky’, may now attract experienced directors to their boards. The incoming directors may rely upon safe harbour protection to avoid the personal risk that comes with accepting such an appointment. The reforms also create enormous investment opportunities as new or struggling businesses can source capital or seek to consolidate with competitors or vertically integrate with their peers. The goal is to increase innovation and build a stronger more resilient economy – 2018 will be an interesting year as the reforms are set in practice.

6 thoughts on “Avoiding Failure – Smaller and Family Businesses”

Comments are closed.