The laws are changing to allow directors to attempt a turnaround or restructure outside of a formal insolvency regime – however, it is important that directors seek advice on the potential recovery provisions that are available to a liquidator should the directors plans fail.

Directors Safe Harbour Protection from Insolvent Trading Personal Liability

The Treasury Laws Amendment (2017 Enterprise Incentives No. 2) Bill 2017 introduced a Safe Harbour Protection for Directors from insolvent trading personal liability. This became effective on 19 September 2017.

New section 588GA introduced a carve-out to section 588G(2) of the Corporations Act 2001 (Cth) and directors can avoid civil liability for insolvent trading on debts if, after insolvency is suspected, the directors initiate a course of action that is reasonably likely to lead to a better outcome for the company (than traditional insolvency administration).

Importantly, this reform is not a “free pass” for directors, who must continue to carefully oversee the solvency of firms. The safe harbour will apply only under certain circumstances and is subject to compliance with tax reporting and employee entitlement obligations.

Extract: “Advocacy: Is Safe Harbour a Safe Bet?” Matthew McGirr, Policy Adviser, AICD

Continuing to trade the business and recover from insolvency – prepare for the worst case scenario

- Should the company meet the thresholds and be able to enter the Safe Harbour, formal insolvency ‘Recovery Provisions’ must still be considered when developing the ‘reasonable’ restructuring and turnaround strategies. This is for the purposes of planning for a worst case scenario. Preserving the value of a business’s goodwill and assets improves the chances of a sale at a later stage.

- Where turnaround strategies fail, there are Recovery Provisions available to a registered liquidator for the claw-back of monies in the period prior to their formal appointment in the insolvency proceedings (through voidable transactions). In planning for the worst case scenario, you need to ensure that you have considered these provisions so as not to cause irreparable disruption to stakeholders that are key to the businesses goodwill (a business can survive formal insolvency and may even be bought back by former owners or management – nothing prevents a company’s legal phoenix). Furthermore, knowledge of these Recovery Provisions may help to prevent the clawback of monies from directors personally and other related parties.

- The Recovery Provisions serve the ‘pari-passu’ principle (which literally means ‘on equal footing’), where all creditors are required to be treated fairly in subsequent distributions from the estate realised by the registered liquidator. It should be noted that the Recovery Provisions below do not provide an exhaustive list of legislative or practical matters to be factored into the restructuring and turnaround strategies.

Insolvency Law Reform Act 2016 (“ILRA”)

In February 2016, the ILRA became law. The ILRA consolidates the rules which govern both corporate and personal insolvencies, which are were split between the Corporations Act 2001 (Cth), the Bankruptcy Act 1966 (Cth) and the Australian Securities and Investments Commission Act 2001 (Cth). The principal practical effects of the new Act are:

- increased alignment of the procedural rules for personal and corporate insolvencies;

- increased regulatory powers of the corporate regulator;

- improving creditor oversight and engagement; and

- insolvency practitioner remuneration.

Some commentators have suggested that the ILRA will make insolvent trading claims against directors much harder to pursue.

The Recovery Provisions

- Division 2 of Part 5.7B is to ensure that unsecured creditors are not prejudiced by the disposition of assets or the incurring of liabilities by a company in a period shortly before the winding up which would have the effect of favouring certain creditors or other persons, and especially related entities.

- This might occur where a creditor was paid out in full rather than having to prove for a proportion of the debt in the winding up (irrespective of whether that creditor has some connection to the company).

- The provisions also seek to avoid transactions where the body of unsecured creditors might be prejudiced by the company having given away assets or incurred liabilities without adequate consideration passing to the company.

Anterior Period = Timescale prior to Formal Insolvency Appointment

- The ‘Anterior Period’ is the time period prior to insolvency appointment and counts back from the ‘Relation-back Day’ (refer to later in this article for explanation).

- This may include the term coined as the ‘Twilight Zone’ that businesses find themselves in when financial difficulties are identified.

- The twilight zone is the point at which a director realises the company faces immediate financial difficulties or may soon face financial difficulties.

Unfair preferences (s588FA)

Anterior period:

- 6 months ending on the relation-back day, or, after that day but on or before the day when the winding up commenced.

- Extended to 4 years where the creditor is a related entity – s588FE(2) & (4).

Conditions (burden of proof is with the liquidator):

- The company must have been insolvent at the time of the transaction or was rendered insolvent as a result of the transaction.

- The company and the creditors are parties to the transaction and a debtor creditor relationship must exist.

- The creditor was preferred by receiving more, in monies or monies worth, than it would have received if it had claimed in the in the winding up and the transaction had not taken place.

Exception – running accounts

- Running accounts arise in a situation where goods are supplied to a company which pays on a running account. Payments are made without any differentiation between past and future goods supplied. These are exceptional under S588FA(3).

Uncommercial transactions (s588FB)

May occur when a company:

- gives a gift to a party for no consideration

- undertakes a burden for no consideration

- sells property at an amount below market value

- agrees to pay for services or property at a significantly greater amount than market value

Anterior period:

- 2 years ending on the relation-back day.

- Extended to 4 years where the creditor is a related entity – s588FE(3) & (4).

Conditions (burden of proof is with the liquidator):

- The company must have been insolvent at the time of the transaction or was rendered insolvent as a result of the transaction.

- It may be expected that a reasonable person in the company’s circumstances would not have entered into the transaction, taking into account the benefits for the company, the detriment to the company, the respective benefits to other parties to the transaction, and any other relevant matter.

Unreasonable director related transactions (s588FDA)

The provision is directed towards preventing companies from making excessive payments or bonuses to directors prior to liquidation.

Anterior period:

- 4 years ending on the relation-back day, or, on or before the day when the winding up commenced.

Conditions:

- The transaction must be made for the benefit of a director or “close associate’ of a director

- The transaction must be unreasonable from the point of view that a reasonable person in the company’s circumstances would not have entered into it on the basis of:

- the respective benefits, costs or detriment to the company

- benefits to the other parties or recipient

- any other relevant matter

Parameters & Relevant Factors Explained

In reading the above, there are some critical technical points that need to be understood. The ‘Relation-back Day’ is discussed separately below.

Related entity

As can be seen above, where the transaction was with a related entity it is extended. The term related entity is defined in s9 and can be summarised as entities with common controllers or individuals who are connected by blood or by law. In relation to a company this also includes a promoter. The rationale behind this is that due to directors inside influence and control, they may influence related party transactions to safeguard their own interests outside of the standard anterior periods. The view of the Harmer Report was that related entities should not be treated equally because they are more likely to have knowledge of the company’s financial affairs and so may be in a position to exert influence over controllers.

‘Void’, not ‘voidable’

—Circulating security interest created within 6 months before relation-back day (s588FJ)

This provision exists to effectively prevent failing companies from creating floating charges to secure past debts, unfavourably to the interests of the general body of creditors.

If the conditions are met, the charge is void and not voidable (as with the other provisions described above), except to the extent that it secures the following:

- an advance paid to the company, or at its direction, at or after that time and as consideration for the circulating security interest; or

- the amount of a liability under a guarantee or other obligation undertaken at or after that time on behalf of, or for the benefit of, the company; or

- an amount payable for property or services supplied to the company at or after that time; or

- interest on an amount above so payable.

—S468 Avoidance of dispositions of property, attachments etc.

The effect of s468 is that once a winding up commences, no property can be validly disposed of unless it is validated by the court. Dispositions are automatically void.

Under s588FJ, the charge is automatically void and it does not require action to be initiated by the liquidator. This is the same for dispositions of property after commencement under s468. The provisions under ss588FJ and s468 may not be considered as clawback provisions as, if found to be void, they are treated as never having occurred.

‘Insolvent Transactions’ & ‘Presumptions of Insolvency’

Insolvent transactions related only to unfair preferences, uncommercial transactions and transactions obstructing creditors’ rights. As the burden of proof lies with the liquidator, proving insolvency can be difficult in some circumstances. In order to assist the liquidator, there are presumptions outlined in s588E.

Including presumptions of insolvency where:

- Insolvency has already been proven in other recovery actions.

- Adequate accounting records have not been kept or have not been retained for 7 years.

- Insolvency has already been proven in other proceedings at point in time 12 months preceding the relation-back day (insolvency is continually presumed from that point until the relation-back day).

The presumption only applies to an unfair preference where the beneficiary is a related entity of the company. The presumption will not apply in circumstances where records were accidentally destroyed, or concealed or removed without the company being implicated.

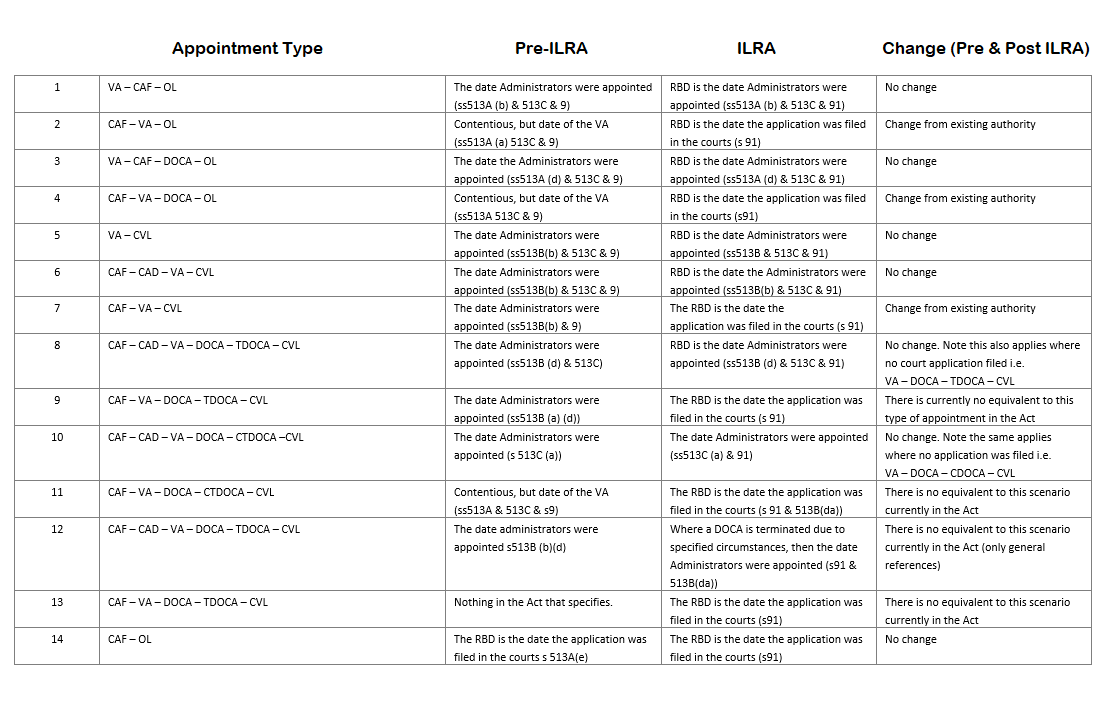

Relation-back Day

Registered liquidators and the Courts use the ‘Relation-back Day’ (s9) to determine what date to use in the clawing-back of voidable transactions (pursuant to ss588FE & 588FF).

Section 91 of the Insolvency Law Reform Act 2016 (Cth) introduced a means for registered liquidators to identify what the relation-back day will be in each formal insolvency circumstance.

A user reference guide is provided in the table below:

LEGEND

Should you require further information, please contact us for an obligation free consultation.

![]()

![]()

![]()

1 thought on “Recovery Provisions – Trading a Business out of Financial Difficulty ”

Comments are closed.